First, let me start off by saying that I never wanted to start a blog. I thought that there were enough blogs out there and that mine would just be more noise in a sea of… well, noisiness. But it turns out that I have a few things to say, so even if no one ever reads this, that’s okay because I’m doing it for me. (I’m actually hoping that at least one or two people tune in, though, because maybe I’ll be able to help them. Like you! You there! How I can help you?)

In 2016, I started to get my shit together. The previous few years were some difficult years for me (read: apocalypse of epic proportions), but 2016 was going to be MY YEAR. (I think my cousin told me this. I probably laughed at the time, but thanks, Danya — you were right!)

I started meditating, exercising regularly and stumbled on the concept of financial independence. If you haven’t heard of it, financial independence is where you save money instead of spending it all so that you can get to a point where you don’t have to work. all. the. time. Don’t get me wrong — I like to work. I just also like to do a lot of other things.

So I paid off all my debt (bye bye student loans!) and started a real big-girl emergency fund. At this point, I’m almost fully-funded with six months of living expenses. I’ve been keeping track of my finances daily and monthly and am feeling good about my future.

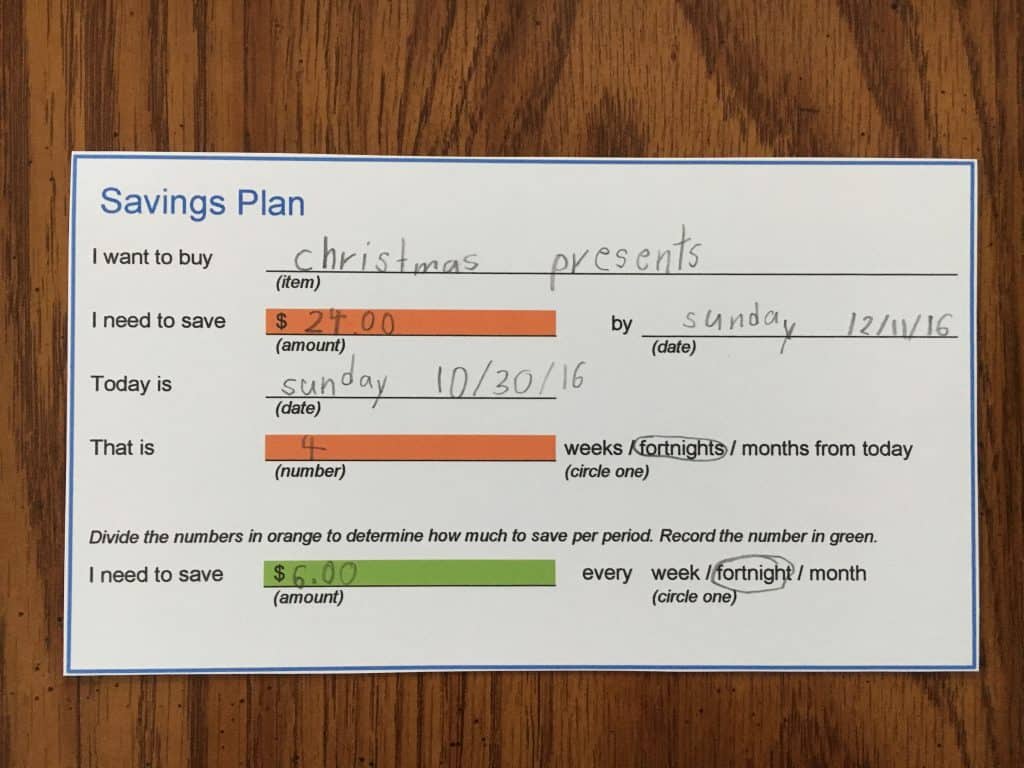

Thinking more about it, I thought I should probably start to teach my son about money so that he would be in a better place at 37 than I am. I’m fortunate that at 8, he’s a captive audience. He’s also pretty good with addition and subtraction and likes money (and toys. And pizza. And talking. He’s a pretty happy kid overall.)

Which brings me here. We live in such an information-saturated time (I’m looking at you Internet) that there are SO many good ideas to choose from. Have you been on Pinterest lately? Unfortunately, there is also a lot of garbage to sift through. Being a researcher at heart, my plan is to dive in and learn everything I can. Then I’ll surface with all the good stuff and post it here.

So if you have little ones, or just want to get YOUR shit together, stop in. I’ll give you the best of what I find and show you what works for us.

Before I go, I want to note that I’m not about saving every penny at the expense of living today. I don’t want to be miserable right now so that I can be free some day in the future. I also am not for rampant consumerism or working a lot so that I can buy a lot of fancy cars, houses, the latest gadgets and mountains of stuff. You’ll soon learn that I’m not a big fan of stuff. My main goal is to be able to live the life I want to live, with all the good parts — friends, relationships, quality time, personal improvement, creativity — the list is endless.

Whew! If you got this far, thanks for reading. I hope to see you again soon!